Normally, the Quarterly is accompanied by a “What I’m Looking For” section in bullet form after the main article.

With 2025 arriving and the potential for changes with the (new?) incoming Trump administration, I’m going to combine the “What I’m Looking For” concept with another common new-year trope to present you with the definitive SolarKal Quarterly Top 25 Predictions for 2025.

These are 100% guaranteed to be at least 50% wrong by year-end or your proverbial money back!

As an aside...

I do wish I had done this last year, as I can attest that where we are today is not quite where I thought we’d be back when we were heading into 2024.

(Disclaimer: These predictions are the author’s and not representative of SolarKal.)

Let’s start with our tentpole topics and see what our 2025 crystal ball says!

1. The solar ITC remains intact.

After months of will they/won’t they, solar incentives end up unchanged, though the low-to-medium income (LMI) adder almost gets chopped.

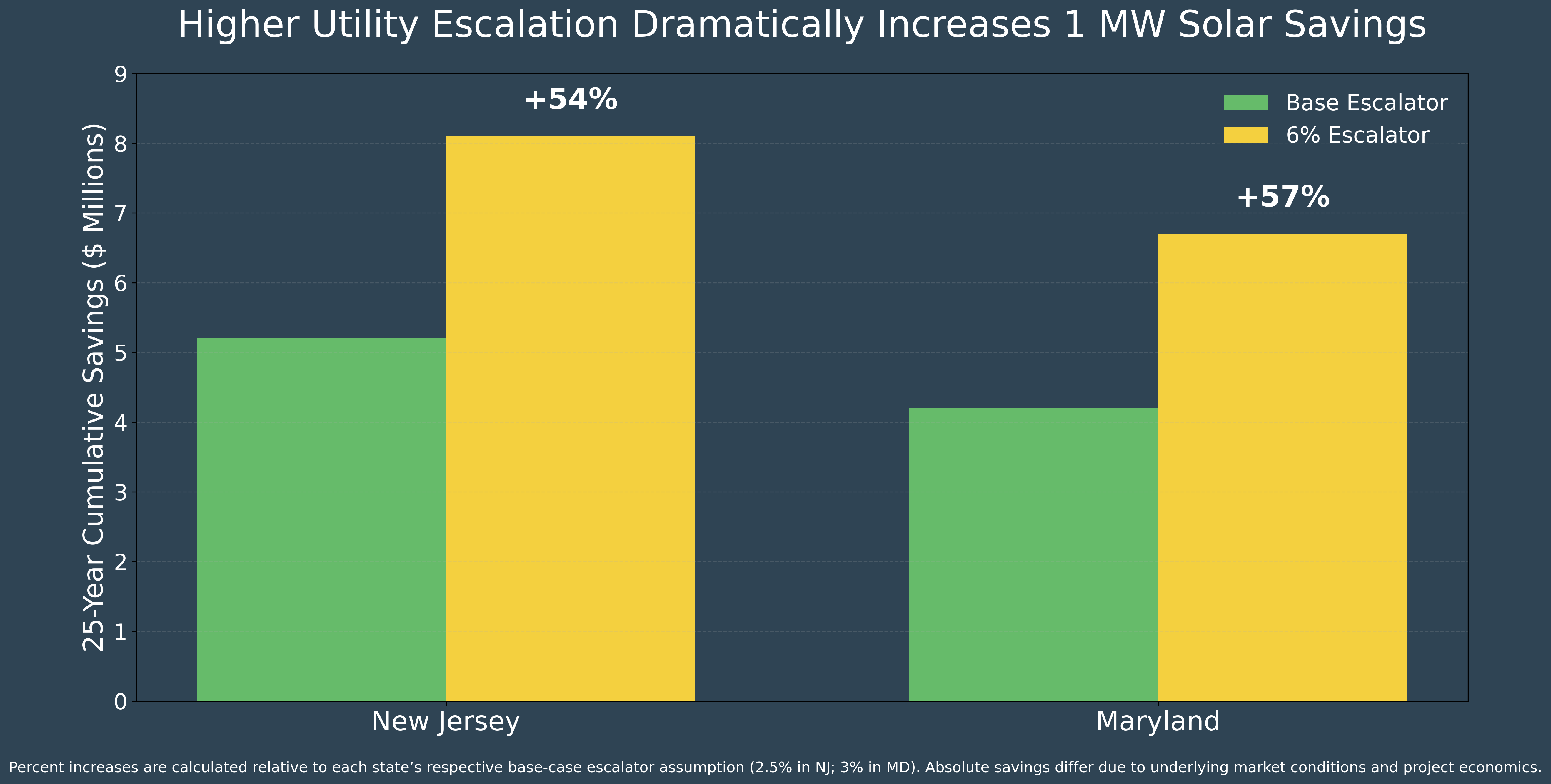

2. Yet it’s not all sunshine — tariffs are higher but not entirely where you’d think.

Tariffs on Chinese panels increase to 50% on Jan. 1 (via the Biden administration) but stay there.

3. Other panels (i.e., Southeast Asia) incur an additional 20% tariff from the Trump administration.

4. As panels make up just ~25% of the cost of systems, the additional tariffs don’t dent solar adoption rates significantly.

(2016-2020 is not discernible here and Biden kept many tariffs).

5. Interest rates remain relatively steady (+/- 1% vs. Fed Funds of 4.6%).

Candidly this is more a deference to the status quo than any sort of data-driven opinion; if I really had a crystal ball for this, I’d probably be in a different job …

6. Interconnection delays are the most cited challenge to further solar procurement.

Okay, sure, this is a gimme.

7. 43 GW installed in 2025.

EIA estimates are at 43 GW in 2025, and I’m betting the current uncertainty pushes more projects to start construction to get ahead of any potential changes. Over.

8. 250 GW in cumulative installed capacity.

The U.S. hit 200 GW at the end of Q3 2024. To be fair, a lot of this hinges on Q4 2024 and the previous prediction. Over.

9. 63% of new electricity generating capacity will be solar.

(This is based on the EIA’s expectation of 63% for the last few months of 2024.) This figure has risen about 50 percentage points (check out this chart!) over the last decade-plus — which highlights just how dominant solar has been. Over.

10. 57 GW in domestic panel manufacturing capacity by year-end.

Higher tariffs encourage U.S. capacity, but gains are offset by 1Q policy uncertainty. Either way, this is an incredible number considering we were at just 15 GW in 2022 and zero in 2019! Under, but not by much.

11. 300K people in the solar industry.

We’re at 280K today, but that’s just 6% more than last year’s 264K (though 2023 was up 14% from 2022). 300K would represent 7%, which is reasonable, but color me cautious on this one — systems have long development and deployment curves, so changes take a while to manifest. Hiring/employment is more sensitive. Under.

12. 3.5 segments out of four post double-digit % YoY increases.

Of residential, commercial, community solar, and utility, all but resi posted double-digit % gains in 2024. Resi is the most susceptible to interest rates and policy uncertainty, which will probably still be headwinds in 2025, and at least one other segment likely straddles the line. Under.

13. 500 MW in average quarterly commercial solar added.

2024 is on pace for an average of 465, while 2023 averaged 390. I have an unfounded hunch to take the under, but I’ll endeavor to be consistent. Over.

14. 40% of the U.S. population lives in a state with a 100% clean portfolio standard.

Today, we are at 38% in 15 states, led by CA, NY, NJ, IL, VA, and MA. This group of 15 has a consistent population, which means more states would have to join to hit 40%. Under.

15. Massachusetts is a major player in 2H 2025.

MA is in the midst of revamping and improving its SMART program. Current expectations are for the program to be in effect by YE 2025, and capacity is already lining up, so get ready — now! Yes, “major player” is a bit undefined, but this is mostly an optimistic prediction on timing rather than the definition of “major.”

16. California’s NEM 3.0 gets pared back by the CA Supreme Court.

File this one in “unlikely,” but the CA Supreme Court agreed to hear a challenge to NEM 3.0, which reduced NEM 2.0 net metering rates for system owners. Again, odds seem against any substantive changes.

17. Speaking of California, the ordered revamp of existing community solar programs doesn’t move the needle.

In June 2024, the CPUC voted against adopting the long-awaited community solar program, instead choosing to update legacy programs. This limits options for buildings without on-site load. However, as energy rates continue to skyrocket, PPA/lease hybrid options are still very lucrative if there is on-site load!

18. New Jersey cracks the top 5 on the Community Solar Leaderboard

(the state is currently #6 behind Colorado).

19. At least one of these states earns a coveted SolarKal “Top Rooftop Community Solar Markets” designation:

Pennsylvania, Minnesota, Colorado, Virginia, Delaware. I have no power over this designation; that belongs to our dedicated and amazing Policy Team!

20. Data centers are the number one driver of corporate solar adoption.

Tech companies that own or lease data centers tend to have commitments to source power for AI from clean energy. Deloitte estimates that DCs will drive more than 57 GW by 2030 alone. Wow!

21. Meta, Amazon, and Google expand the gap between themselves and #4 on solar capacity lists.

Currently, the three are well clear of #4 (Apple), but this gap will expand.

22. Amazon takes #1 from Meta.

Amazon has a pipeline of 13 GW of solar, just less than half of the entire top 10. Meta is second at 6 GW.

23. At least two companies fall out of the top 10.

Don’t ask me who, but I’d guess Cargill, with Prologis as a dark horse.

Happy Holidays!

24. The unstoppable solar transition notches another year of gains.

25. Exactly 15 of these predictions turn out to be correct.